Market Overview:

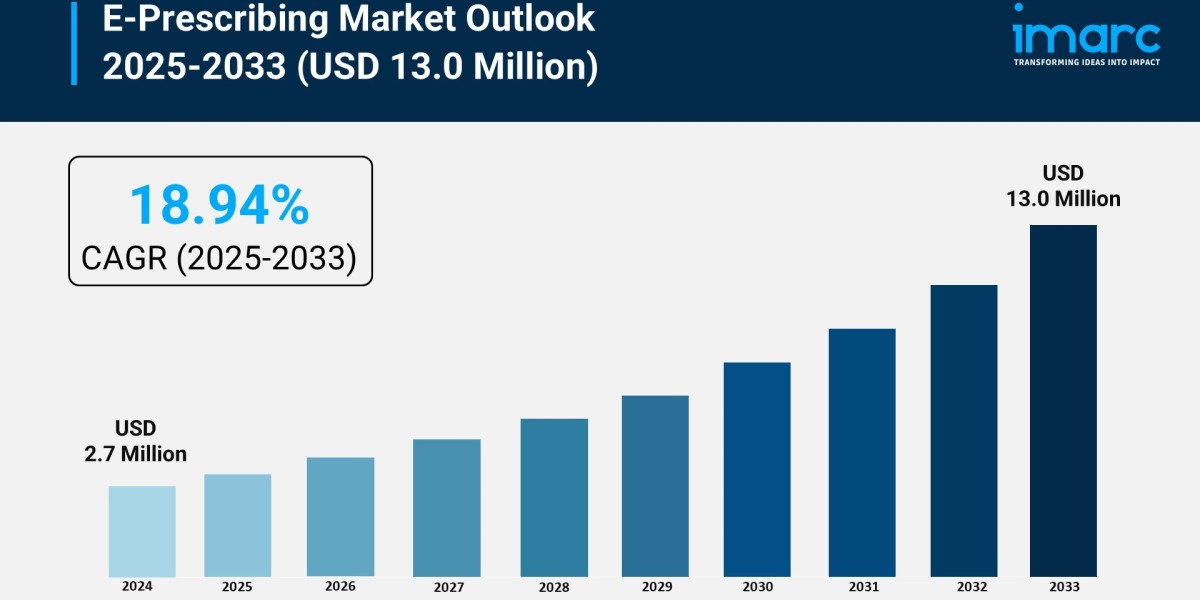

The e-prescribing market is experiencing rapid growth, driven by regulatory mandates for digital prescription adoption, focus on reducing medication errors and improving patient safety, and escalating need for healthcare cost containment and efficiency. According to IMARC Group's latest research publication, "E-Prescribing Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033", the global e-prescribing market size reached USD 2.7 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 13.0 Million by 2033, exhibiting a growth rate (CAGR) of 18.94% during 2025-2033.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/e-prescribing-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the E-Prescribing Industry

- Regulatory Mandates for Digital Prescription Adoption

Government initiatives globally are a primary catalyst for the widespread adoption of e-prescribing systems, often driven by the urgent need to address public health crises and optimize healthcare delivery. For instance, in the United States, specific federal acts have mandated the electronic prescribing of controlled substances (EPCS) for drugs covered by major government health programs, significantly driving market penetration. This legislative push is mirrored in other major economies, such as the United Kingdom's National Health Service (NHS), which reported that nearly 95% of all medicine prescriptions were made using electronic means in a recent reporting period. Such mandates compel healthcare providers, from large hospitals to small physician practices, to invest in e-prescribing solutions, thereby standardizing workflows and creating a robust, interconnected digital prescription network. This regulatory enforcement is a powerful non-market mechanism accelerating market growth.

- Focus on Reducing Medication Errors and Improving Patient Safety

A fundamental driver of e-prescribing growth is its proven ability to enhance patient safety by reducing the prevalence of medication errors inherent in paper-based systems, such as illegibility, transcription mistakes, and drug-to-drug interactions. Integrated e-prescribing platforms often include sophisticated Clinical Decision Support (CDS) tools that automatically check for potential adverse drug events, allergies, and appropriate dosing at the point of care. For example, a major industry player recently introduced a feature that enhances prescriber-patient communication by allowing doctors to contact patients via their personal mobile devices without revealing private contact information, displaying a customizable office number instead. The quantifiable impact on workflow is also significant: e-prescribing lowers pharmacy callback rates for clarification by approximately 40%, directly improving staff productivity and safety across the healthcare continuum.

- Escalating Need for Healthcare Cost Containment and Efficiency

The relentless pressure on healthcare systems worldwide to contain costs while maintaining high-quality care is strongly fueling the e-prescribing market. By digitizing and streamlining the prescription process, healthcare organizations realize substantial administrative cost savings. The system reduces costs associated with printing, faxing, handling, and manually processing prescriptions. Furthermore, electronic solutions can integrate with pharmacy benefit managers to instantly display cost-effective alternatives and generic substitutions at the time of prescribing, directly lowering patient out-of-pocket expenses. This efficiency gain also extends to controlled substances; the use of Electronic Prescribing for Controlled Substances (EPCS) helps reduce fraud and misuse, addressing a critical public health and financial burden. The total overhead related to prescription prior authorizations, often simplified by e-prescribing, is estimated to cost billions of dollars annually.

Key Trends in the E-Prescribing Market

- Deep Integration of AI and Machine Learning in CDS

A major emerging trend is the incorporation of advanced Artificial Intelligence (AI) and Machine Learning (ML) algorithms into Clinical Decision Support (CDS) within e-prescribing systems. This moves the technology beyond simple alerts to predictive and personalized insights. Concrete examples include AI models that analyze a patient's historical data, genetics, and real-time lab results to recommend optimized dosages, proactively flag complex drug-disease interactions, and even predict potential patient adherence issues before the prescription is filled. In the specialty drug segment—which requires precise dosing for complex, high-cost treatments like those for cancer or autoimmune diseases—e-prescribing systems are being customized to configure dosages based on patient-specific factors such as weight or lab values, significantly improving therapeutic accuracy and minimizing waste of expensive medication.

- Widespread Adoption of Cloud-Based Solutions

The transition from on-premise to web and cloud-based e-prescribing platforms is an undeniable trend shaping market structure. Cloud solutions offer superior scalability, accessibility, and lower upfront investment costs, making them particularly appealing to small to medium-sized practices and clinics. One major data point shows that the web/cloud-based delivery segment accounted for over 74% of the market share in a recent analysis period, highlighting its dominance. This shift allows providers to securely access patient and drug information from nearly any location with an internet connection, which is crucial for the growth of telehealth and remote patient monitoring. Furthermore, cloud-based systems enable automatic software updates and continuous security patching, removing the administrative burden from healthcare providers and ensuring compliance with evolving data privacy standards.

- Expansion of E-Prescribing for Controlled and Specialty Drugs

The market is witnessing a strong shift towards expanding the use of e-prescribing for complex prescription types, particularly controlled substances and high-cost specialty medications. The need to combat prescription fraud and the opioid crisis is accelerating the adoption of Electronic Prescribing for Controlled Substances (EPCS), which provides an auditable, secure, and clear chain of custody. Controlled substances recently accounted for over 38% of the total prescription volume processed by a major e-prescribing network. Simultaneously, the specialty drug segment is poised for rapid expansion, growing at a significant rate in the current market. These specialized e-prescribing systems include built-in workflows for prior authorization, financial assistance program enrollment, and comprehensive patient monitoring plans, streamlining the complex process of managing these critical therapies.

Leading Companies Operating in the Global E-Prescribing Industry:

- Allscripts Healthcare Solutions Inc.

- Athenahealth Inc. (Veritas Capital and Evergreen Coast Capital)

- Cerner Corporation

- Computer Programs and Systems Inc.

- DrFirst.com Inc.

- Epic Systems Corporation

- Henry Schein Inc.

- Medical Information Technology Inc.

- Nextgen Healthcare Inc.

- Surescripts LLC

E-Prescribing Market Report Segmentation:

By Component:

- Solutions

- Services

Solutions accounts for the majority of shares due to rising demand for comprehensive e-prescribing platforms with integrated safety features.

By Delivery Mode:

- Web-based

- Cloud-based

- On-premises

Web-based dominates the market due to accessibility and cost-effectiveness for healthcare providers.

By End User:

- Hospitals

- Pharmacies

- Office-based Physicians

- Others

Hospitals represents the largest segment owing to high patient volumes and complex medication management requirements.

By Specialties:

- Oncology

- Sports Medicine

- Neurology

- Cardiology

- Others

Oncology accounts for the largest market share due to complex medication regimens requiring specialized prescription management.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

North America enjoys the leading position owing to advanced healthcare IT infrastructure and supportive government regulations.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302