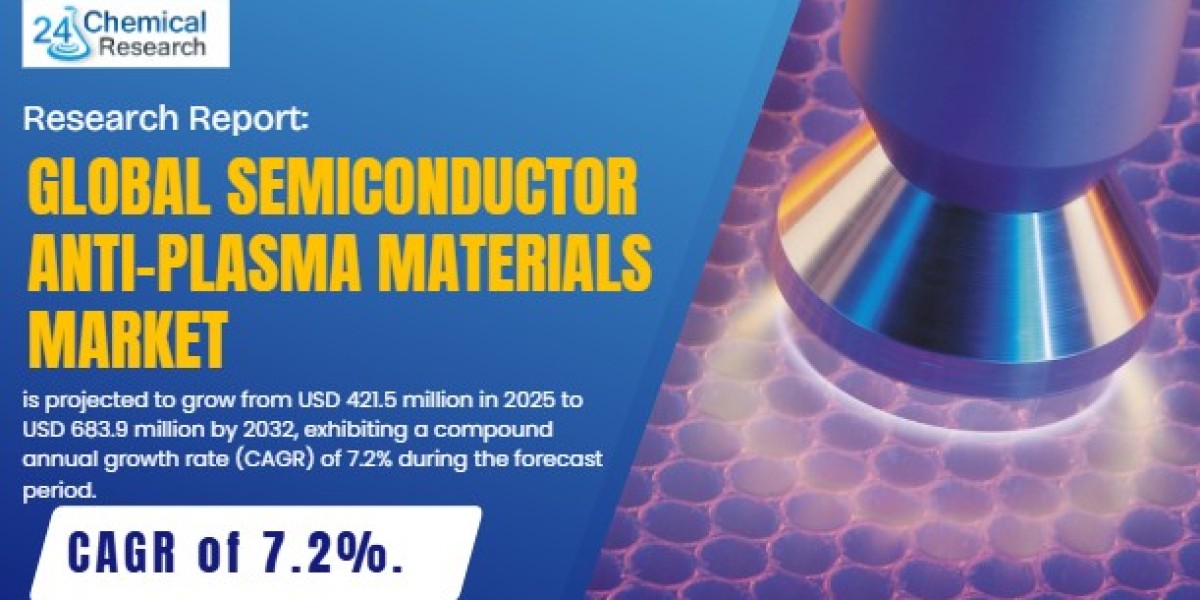

This robust expansion is fueled by the critical need for materials that can withstand extreme plasma environments in semiconductor manufacturing processes. The market's growth trajectory underscores the essential role of specialized materials in enabling advanced node semiconductor production and ensuring manufacturing tool component longevity.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/188052/global-semiconductor-antiplasma-materials-forecast-market

Top 7 Emerging Trends in the Semiconductor Anti-Plasma Materials Industry

Several noteworthy developments are shaping market performance between 2025 and 2032:

- Transition to Advanced Node Semiconductor Manufacturing: Increasing demand for materials capable of withstanding higher plasma densities and temperatures in sub-7nm and 3nm chip production.

- Rise of Yttrium-Based Ceramic Coatings: Growing adoption of yttrium oxide and other rare-earth ceramics offering superior plasma erosion resistance compared to traditional materials.

- Expansion in Etch and CVD Chamber Components: Rising consumption of anti-plasma materials for critical components including focus rings, showerheads, chamber liners, and wafer clamps.

- Compound Semiconductor and Power Device Growth: Increasing material requirements for GaN and SiC power semiconductor manufacturing processes.

- Advanced Coating Technologies: Development of specialized coating methods including plasma spray, ALD, and CVD techniques for enhanced film density and adhesion.

- Material Innovation for EUV Lithography: Development of plasma-resistant materials compatible with extreme ultraviolet lithography systems.

- Sustainability and Recycling Initiatives: Growing focus on component refurbishment, recoating services, and circular economy approaches to reduce cost and environmental impact.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/188052/global-semiconductor-antiplasma-materials-forecast-market

Key Market Drivers

Key growth factors contributing to the semiconductor anti-plasma materials market expansion include:

- Global Semiconductor Capacity Expansion: Massive investments in new semiconductor fabrication facilities worldwide, particularly in the United States, Taiwan, and South Korea.

- Increasing Process Complexity and Plasma Intensity: Transition to more aggressive etch and deposition processes requiring enhanced material performance.

- Demand for Higher Component Lifespan: Need for materials that reduce particle generation, maintenance frequency, and overall cost of ownership.

- Growth in 3D NAND and DRAM Manufacturing: Expanding memory chip production driving consumption of plasma-resistant components.

- Advanced Packaging Technologies: Rising adoption of fan-out wafer-level packaging and 3D integration requiring specialized plasma-resistant materials.

Strategic Developments

Market participants are pursuing several strategic initiatives:

- R&D Investments in Advanced Ceramics: Significant research funding directed toward developing next-generation alumina, yttria, and quartz-based materials.

- Vertical Integration Strategies: Companies expanding capabilities across material synthesis, component manufacturing, and coating services.

- Strategic Partnerships with Equipment OEMs: Collaborative development agreements with semiconductor equipment manufacturers for application-specific solutions.

- Geographic Expansion to Support Fab Projects: Establishment of local technical support and manufacturing near major semiconductor cluster regions.

Technological Advancements

Recent technological progress is enhancing material performance and capabilities:

- Nano-Structured Ceramic Coatings: Development of nano-crystalline and composite coatings with improved erosion resistance and thermal stability.

- Advanced Quartz Formulations: Innovation in high-purity, doped quartz materials offering enhanced plasma resistance for etch applications.

- Precision Manufacturing Technologies: Implementation of advanced machining and finishing techniques for complex component geometries.

- Predictive Lifetime Modeling: Development of AI-based models predicting component lifespan and optimizing maintenance schedules.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/188052/global-semiconductor-antiplasma-materials-forecast-market

Regional Insights

The semiconductor anti-plasma materials market demonstrates distinct geographic patterns:

- Asia-Pacific: Dominates the global market, driven by concentrated semiconductor manufacturing in Taiwan, South Korea, China, and Japan.

- North America: Significant market with strong growth prospects, supported by major fab investments in the United States and presence of key equipment manufacturers.

- Europe: Established market characterized by specialty material expertise and research capabilities in advanced ceramics.

- Southeast Asia: Emerging growth region supported by semiconductor backend and packaging operations in Malaysia, Singapore, and Vietnam.

Key Companies

The competitive landscape includes specialized material suppliers and diversified chemical companies:

- CoorsTek, Inc. (US)

- Kyocera Corporation (Japan)

- Morgan Advanced Materials (UK)

- Momentive Performance Materials (US)

- Ferrotec Corporation (Japan)

- Tosoh Corporation (Japan)

- AGC Inc. (Japan)

- Plansee SE (Austria)

Get Full Report Here: https://www.24chemicalresearch.com/reports/188052/global-semiconductor-antiplasma-materials-forecast-market

Market Perspective

The global semiconductor anti-plasma materials market is positioned for strong growth, underpinned by the fundamental expansion of semiconductor manufacturing capacity and increasing process intensity. As chip manufacturers push the boundaries of Moore's Law and adopt new materials, the demand for advanced plasma-resistant solutions is expected to accelerate through 2032. Material suppliers focusing on innovation, reliability, and cost-effectiveness will be best positioned to capitalize on the significant opportunities in this critical segment of the semiconductor supply chain.

Contact Us:

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch