Introduction

The Biomarkers Market includes the discovery, validation, development, regulatory qualification, and commercial use of measurable biological indicators applied to detect diseases, monitor therapeutic outcomes, predict clinical responses, and guide medical decision-making. Biomarkers can originate from genes, proteins, metabolites, enzymes, cells, or digital physiological signals collected through advanced diagnostic platforms.

Biomarkers hold strategic global importance because modern medicine increasingly focuses on early disease detection and precise treatment planning instead of broad one-size-fits-all models. They influence pharmaceutical development, oncology screening, neurology profiling, infectious disease surveillance, immunology analysis, cardiology assessment, metabolic disease programs, and long-term patient monitoring strategies.

In 2024, the global biomarkers industry is valued at an estimated USD 78 billion. The market’s relevance is supported by rising chronic disease prevalence, increasing clinical trial activity, expanded use of companion diagnostics, and integration into precision medicine models. Biomarkers generate critical data for drug development pipelines and clinical care programs. Their use reduces diagnostic uncertainty, improves patient stratification, supports risk prediction, and assists regulatory decisions during drug approvals and clinical study outcomes. The industry is also gaining commercial value from AI-supported biomarker interpretation and multi-omics profiling.

Learn how the Biomarkers Market is evolving—insights, trends, and opportunities await. Download report: https://www.databridgemarketresearch.com/reports/global-biomarkers-market

The Evolution

Biomarker science has evolved from basic biochemical measures into complex molecular signatures interpreted through digital analysis and computational biology systems.

1980–2000: Early biomarkers were primarily single-protein or enzyme-based measures used in cardiology and immunology. Cholesterol panels, hormone-linked indicators, and inflammation markers became standard clinical tools. These biomarkers served functional roles but offered limited predictive precision.

2001–2013: Human genome research expanded biomarker discovery into DNA, RNA, and genetic sequence-linked indicators. PCR tools matured for infectious disease profiling. Precision oncology research began identifying tumor-specific protein biomarkers. Pharmacogenomic biomarkers entered trials for therapy response prediction.

2014–2019: Multi-omics approaches accelerated innovation. Proteomics, metabolomics, transcriptomics, epigenomics, and lipidomics increased the measurable biomarker pool. Next-generation sequencing (NGS) became cost-efficient enough for clinical research use. Liquid biopsy biomarkers transformed cancer screening, enabling non-invasive tumor DNA detection. AI models started supporting biomarker interpretation.

2020 onward: The medical industry adopted biomarkers to support remote diagnostics, pandemic surveillance, immunotherapy response prediction, neurodegenerative disease staging, toxicology assessment, treatment stratification, and digital biomarker platforms using wearable physiological data feeds. Key construction innovations include high-throughput multi-omics labs, AI-assisted biomarker modeling, cloud-linked bioinformatics, and scalable companion diagnostic modules that pair biomarkers into regulatory pipelines for drug approvals. Demand behavior shifted from traditional lab diagnostics into multiplex, predictive, personalized, high-throughput, AI-supported, multi-omics-led, and digital health-integrated biomarker frameworks.

Market Trends

1. Consumer and Clinical Behavior Trends

Patients increasingly expect diagnostics that provide predictive, personalized risk insights rather than single-factor results.

Pharmaceutical developers prioritize biomarkers that support companion diagnostics for targeted therapies.

Hospitals invest in platforms enabling biomarker-led treatment stratification for faster decisions.

2. Technology Adoption

Multi-omics testing platforms show fast adoption in clinical research and diagnostic labs.

Artificial intelligence improves detection accuracy and reduces false-positive interpretations.

NGS sequencing accelerates validation of genomic biomarkers.

Liquid biopsy platforms expand non-invasive cancer biomarker screening.

Mass spectrometry adoption increases sensitivity for metabolite biomarkers.

3. Regional Adoption Patterns

North America leads adoption, driven by strong clinical research and precision drug approval pipelines.

Europe shows fast uptake in oncology profiling and regulatory qualification programs.

Asia-Pacific records the highest growth rate, driven by expanded diagnostics and rising R&D investments in China, Japan, South Korea, India, and Singapore.

Latin America is expanding biomarker-informed clinical trial pipelines in Brazil, Mexico, Argentina, and Chile.

Middle East & Africa show emerging adoption due to investments in genomic sequencing and oncology biomarkers.

4. Market Priority Areas

AI-supported biomarker interpretation

Companion diagnostics

Cancer multiplex panels

Immunotherapy response prediction markers

Neurology biomarkers for Alzheimer’s, Parkinson’s, MS

Infectious disease molecular biomarkers

AI clinical validation models

Pandemic surveillance biomarker platforms

Drug-response stratification programs

Challenges

Validation complexity creates long qualification timelines for clinical biomarkers.

Regulatory approval paths differ across Europe, North America, and Asia, slowing global synchronization.

High cost of multi-omics profiling and mass spectrometry limits adoption in underserved clinical settings.

Standardization issues in sample handling affect reproducibility.

Biomarker sensitivity limits pose risks for early disease detection benchmarks.

Data interpretation challenges increase false-positive alerts when AI models lack sufficient training.

Market Risks

Clinical evidence inconsistency

Reimbursement uncertainty for predictive biomarkers

Data security risk from cloud-linked bioinformatics

Fragmented approval pathways

Assay interference risks

Limited skilled bioinformatics personnel

False-positive escalations

Sample integrity risks

High logistics complexity for multi-site clinical validation trials

EHS scrutiny for assay chemicals

Insurance costs for diagnostic liabilities increasing after error rates rise

Port congestion delaying import of sequencing reagents and validation equipment

Bottlenecks from transformer-cooling compliance for biomarkers stored in ultra-cold units

Market Scope

By Biomarker Type

Genomic biomarkers (DNA/RNA sequences, mutations, expression profiles)

Proteomic biomarkers (enzymes, receptors, tumor proteins)

Metabolomic biomarkers (lipids, metabolites, small molecules)

Epigenetic biomarkers (DNA methylation, histone alteration)

Immunologic biomarkers (cytokines, immune signatures, inflammation signals)

Digital biomarkers (wearable ECG, glucose monitors, activity and vital feeds for modeling)

Other cell-based and molecular biomarkers

By Application

Oncology (largest share)

Neurology

Cardiology

Immunology

Infectious diseases

Nephrology

Endocrinology

Clinical trials

Companion diagnostics

Personalized medicine

Pandemic surveillance

By Testing Technology

PCR and qPCR platforms

Next-generation sequencing (NGS)

ELISA and multiplex immunoassays

Mass spectrometry

Chromatography systems

Liquid biopsy tools

Wearable physiological digital indicator feeds

AI-clinical biomarker modeling platforms

Regional Scope Comparison

North America: Advanced clinical adoption, regulatory qualification activity, oncology trial dominance.

Europe: Strong precision medicine and oncology screening, fast digital biomarker uptake, sustainability scrutiny.

Asia-Pacific: Highest CAGR due to R&D investments, local qualification hubs, population-driven screening needs.

Latin America: Growing clinical trial adoption, increasing diagnostics in Brazil, Mexico, Argentina.

Middle East & Africa: Emerging genomics, oncology biomarker adoption, modernization investment.

End-User Industries

Hospitals, diagnostic labs, biotech research firms, academic institutes, pharmaceutical clinical trial operators, government health programs, public health surveillance departments, precision medicine clinics, consumer health tech firms, wearables-linked biomarker data providers, ultra-cold logistics operators for reagent storage, regulatory test labs, oncology screening networks, neurodegenerative disease research centers, and digital health cloud platforms.

Market Size and Factors Driving Growth

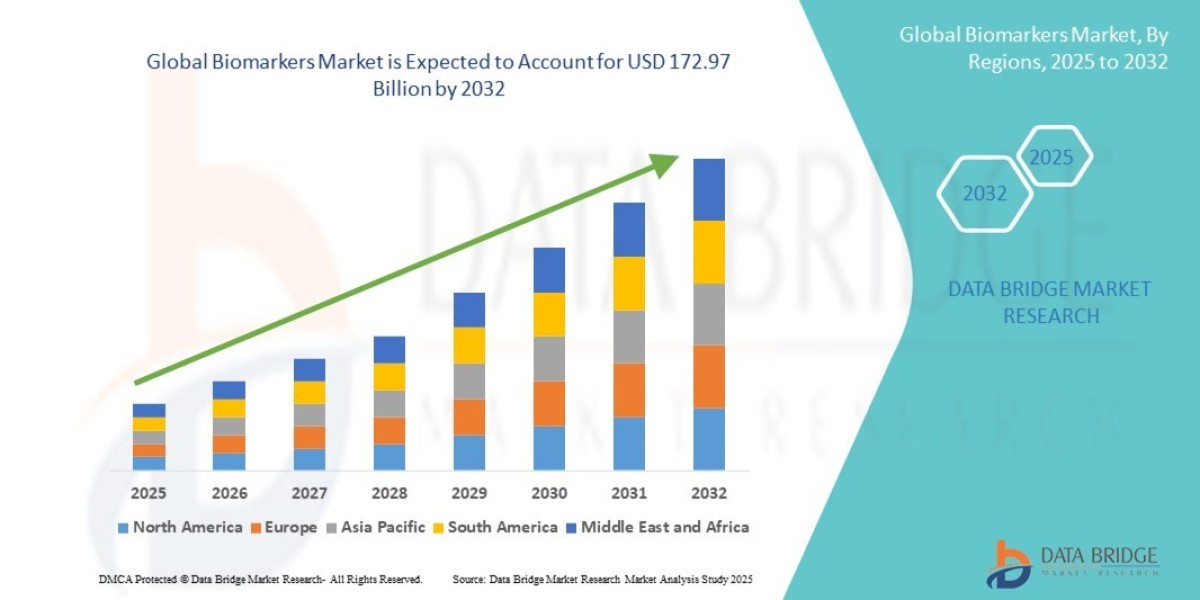

- The global biomarkers market size was valued at USD 56.94 billion in 2024 and is expected to reach USD 172.97 billion by 2032, at a CAGR of 14.90% during the forecast period

Key Factors Driving Growth

Rising chronic disease prevalence: Cancer, cardiology disorders, metabolic diseases, autoimmune conditions, and neurodegenerative illnesses increase screening volume.

Precision medicine adoption: Biomarkers are essential in stratifying patient populations for targeted therapies.

Clinical trial dependence: Pharmaceutical R&D increasingly requires validated biomarker endpoints to support regulatory submissions.

Companion diagnostics growth: Targeted drug pipelines integrate biomarkers for therapeutic eligibility decisions.

Technology cost reduction: NGS, PCR, multiparameter immunoassays, and liquid biopsy modules have become scalable for broad commercial deployment.

AI-interpretation platforms: Machine learning reduces interpretation error rates and enhances predictive value.

Healthcare decentralization: Remote patient monitoring and wearable-sourced digital biomarker datasets support long-term health profiling.

Investment in multiplex panels: Oncology centers and labs seek high-throughput, multivariable biomarker testing.

Drug-response prediction models: Immunotherapy and oncology pipelines rely on response-forecasting biomarkers for early go/no-go decisions.

Data-driven care pathways: Regulatory agencies, payers, and hospitals use biomarkers to reduce uncertainty in clinical decisions.

Regional Growth Opportunity

North America remains the adoption leader due to regulatory-qualified biomarker pipelines and strong colocation of R&D clusters.

Europe leads adoption of oncology and neurology biomarkers due to precision medicine frameworks and environmental compliance requirements for assays and sample storage.

Asia-Pacific shows the fastest scale-up as regional governments invest in population-wide screening programs, oncology profiling, pandemic biomarker surveillance, and local diagnostic reagent production.

Opportunity Channels for Stakeholders

AI-assisted clinical biomarker validation

Cancer multiplex biomarker panels

Liquid biopsy molecular indicator systems

Wearable-derived digital biomarker datasets

Sovereign biomarker qualification hubs

Immunotherapy response predictors

Neurodegenerative staging indicators

PCR-based pandemic biomarkers

Metabolite and lipid marker panels for metabolic disease

Academic and hospital R&D alliances

Cloud-linked biomarker bioinformatics platforms

Scalable reagent-storage and ultra-cold integrity planning

Therapeutic-eligibility companion diagnostics

Eco-certified biomarker programs for sustainable clinical procurement

Conclusion

The global biomarkers market continues to expand due to persistent disease screening requirements, pharmaceutical R&D dependence, companion diagnostics integration, population aging, precision medicine adoption, sensor-sourced digital biomarker feeds, AI-based interpretation, and long-term shifts toward high-throughput multi-omics platforms.

Market sustainability is supported by diagnostic certainty improvements, repeatable laboratory pipelines, standardized sample handling, and evolving regulatory interest in biomarker-qualified endpoints. Stakeholders that invest in scalable biomarker platforms, AI-based qualification, secure cloud bioinformatics, multiplex oncology panels, liquid biopsy clusters, immunotherapy predictions, and neurology staging indicators will support the next period of biomarker commercialization through 2035.

Future stakeholder opportunities include precision drug pipelines pairing biomarkers into companion diagnostics, population-wide cancer and metabolic disease screening, pandemic biomarker surveillance modules, neurology staging programs, and AI-validated molecular assay ecosystems. The long-term outlook remains strong as diagnostics and therapeutic stratification models build increased dependence on qualified biomarkers.

FAQ

What is the Biomarkers Market size in 2024?

The global biomarkers market is valued at USD 78 billion in 2024.What is the projected market size by 2035?

The market is forecast to reach USD 190–205 billion by 2035.What is the expected CAGR (2025–2035)?

The industry is expected to grow at 7.8% CAGR from 2025 to 2035.Which segment holds the largest share?

Oncology biomarkers remain the largest segment.Which regions lead market adoption?

North America leads adoption, Asia-Pacific records the highest growth rate.What testing technologies drive market scale-up?

NGS, PCR/qPCR, multiplex immunoassays, liquid biopsy modules, mass spectrometry, and AI-based biomarker interpretation platforms.- Browse More Reports:

Global Blood and Fluid Warming Medical Devices Market

Global Breast Lesion Guidance Systems Market

Global Buildtech Textiles Market

Global Bulk Bag Divider Market

Global Business Jet Market

Global Canoeing and Kayaking Equipment Market

Global Capillary Blood Collection Devices Market

Global Cardiac Monitoring and Cardiac Rhythm Management Devices Market

Global Check Rails Market

Global Chicory Root Market

Global Chocolate Spreads Market

Global ChloroHydroxyPropylTrimethyAmmonium Chloride (CHPTAC) Market

Global Compostable Plastic Packaging Market

Global Computer Vision AI Camera Market

Global Concrete Reinforcing Fiber MarketAbout Data Bridge Market Research:

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- [email protected]